Blog: The UK merged R&D tax scheme – What you need to know

In the Autumn Statement 2023, the Chancellor announced significant changes to the Research and Development (R&D) tax incentive schemes. A combination of the existing R&D Expenditure Credit (RDEC) and R&D SME schemes into a single, merged scheme. The new scheme introduces an above-the-line credit, which allows companies to claim their qualifying R&D costs, including contracted-out R&D. It also incorporates the more generous SME scheme PAYE and National Insurance contributions cap. However, there are some restrictions on relief for overseas expenditure, which will take effect for accounting periods commencing on or after 1 April 2024.

With the merging of schemes, we are seeing yet another significant change in the world of R&D tax relief schemes. We understand that the past few years have been confusing and challenging for businesses to keep up with the changing landscape. Here at MPA, R&D tax credits are one of the many services we live and breathe. We have created this blog to simplify the changes, but our team of experts are also available to answer any questions regarding how the merged scheme will affect your business.

This blog will cover:

- Why is the merger happening?

- What is the new merged R&D scheme rate?

- What is above-the-line credit?

- Additional tax relief for R&D-intensive SMEs

- PAYE Cap

- Overseas R&D costs & Subcontracting

- What’s next and how can MPA Help?

Why is the merger happening?

The decision to merge the SME R&D tax credit scheme with the RDEC scheme stems from several factors:

Simplification: The merger is primarily aimed at simplifying the R&D tax relief landscape. Having two separate schemes can create complexity and confusion, especially for SMEs. Merging the schemes will streamline the process, making it easier for businesses to access R&D tax incentives.

Consistency: Another reason for the merger is to ensure consistency in the application of R&D tax incentives. The two schemes have different eligibility criteria and calculation methods, which can lead to inconsistencies and inequities in tax relief across businesses. By merging the schemes, businesses will be treated fairly, regardless of size or industry.

Effectiveness: The government hopes that consolidating the two schemes will enhance the effectiveness of R&D tax incentives. A more cohesive approach to supporting R&D activities could lead to increased investment in innovation and ultimately drive economic growth.

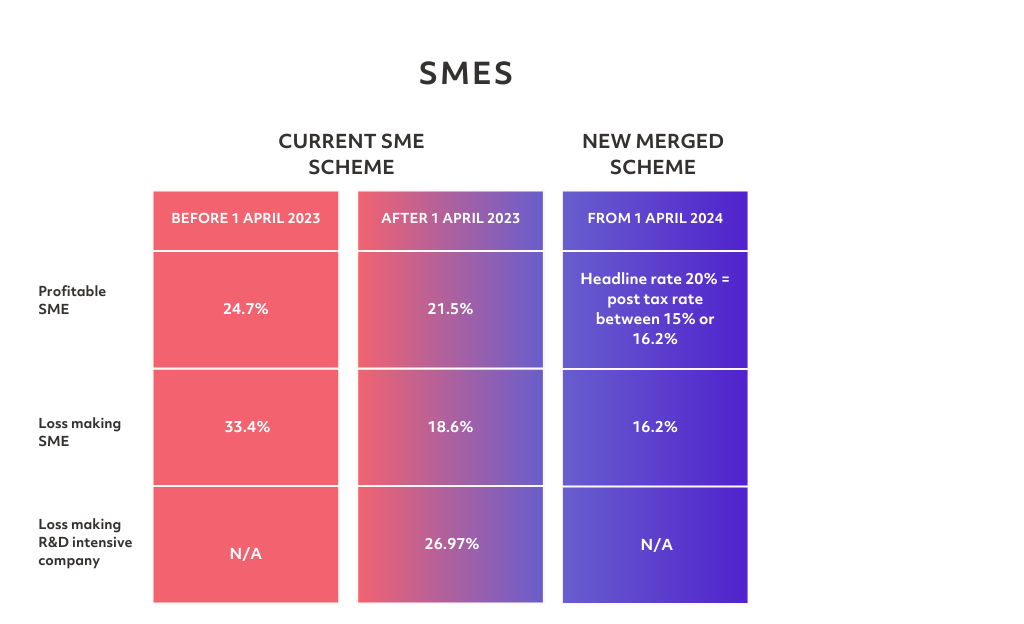

What is the new merged R&D scheme rate?

The tables below show how R&D tax relief rates have changed in recent years. The merged scheme applies for accounting periods beginning on or after 1 April 2024. For businesses submitting claims for accounting periods prior to 1 April 2024, they will need to refer to the previous rates.

What is Above the Line Credit?

With the current RDEC scheme, relief is given via a taxable credit which is currently 20% of the qualifying expenditure – this is recognised in the claimant company’s pre-tax income. The new merged scheme will follow this approach, and this is designed to raise the prominence of the R&D function within a business.

Additional tax relief for R&D-intensive SMEs

The SME intensive that was introduced in the Spring Budget 2023 scheme is going through some changes:

- The threshold for a company to be considered R&D intensive will be reduced from 40% to 30% of total expenditure.

- The government is introducing provisions to enable an intensive SME to claim intensive relief in year two. New rules will be introduced to protect the R&D-intensive scheme from businesses manipulating their intensity by using short accounting periods.

- The government has introduced a one-year grace period to support companies whose R&D intensity falls below 30%. This grace period will be especially helpful for companies whose R&D expenditure fluctuates year on year and may otherwise end up switching between the intensive scheme and the main merged scheme.

- Enhanced R&D Intensive Support (ERIS) is a program that SMEs that are involved in R&D and are operating at a loss to deduct an additional 86% of their qualifying costs. This deduction is added to the 100% deduction that already appears in their accounts, resulting in a total deduction of 186%. Additionally, these SMEs can claim a payable tax credit, which is not subject to tax, and can be worth up to 14.5%.

PAYE Cap

The amount of the PAYE cap for claims under both the merged scheme and ERIS is £20,000 plus 300% of the company’s relevant PAYE and National Insurance contributions liabilities. Under the merged scheme, the PAYE cap (where applicable) limits the amount of payable credit you can receive in the accounting period for which you claim. Any excess over the cap is carried forward and treated as an amount of RDEC to which the company is entitled for the next accounting period. Under ERIS, any claim for tax credit over the cap (where applicable) is invalid. The PAYE cap does not apply if the company is exempt. Further information is available at CIRD90600.

Overseas R&D costs & Subcontracting

Overseas R&D Restrictions:

- Starting from April 1, 2024, expenditure on overseas R&D activities will generally no longer qualify for R&D incentives schemes.

- However, there’s an exception: If the necessary R&D conditions are not present in the UK, but they are in the overseas territory, and it would be wholly unreasonable to replicate them in the UK, then the expenditure may still qualify.

- For contractor payments, the location of the activity determines whether the overseas restriction applies.

- For payments related to externally provided workers (EPWs), it depends on whether the EPW’s earnings are subject to PAYE and Class 1 NICs.

- Claimants don’t need to provide upfront evidence, but understanding the supply chain and apportioning payments to the UK element is crucial.

Exceptions to Overseas R&D Restriction:

- Overseas expenditure on contracted-out R&D and payments for EPWs not subject to UK PAYE/NIC may still qualify if certain conditions are met.

- These conditions include the absence of necessary R&D conditions in the UK.

Qualifying Subcontractor Payments:

- Under the merged R&D scheme, all companies can claim qualifying subcontractor payments.

- The principal condition is that at the time the contract was entered into, the subcontractor was intended or contemplated to undertake R&D to satisfy the contract.

- If a subcontractor unexpectedly undertakes R&D while delivering the contracted product or service, it can still potentially claim R&D relief.

What’s next and how can MPA Help?

As one of the UK’s leading specialists in tax consultancy, we at MPA are not just observers of the evolving R&D landscape but active champions, constantly striving to maximise the benefits for innovative businesses. With the recent announcement of significant changes to the R&D tax incentive schemes, including the merging of RDEC and R&D SME schemes, we’re at the forefront of providing clarity and guidance in navigating these transformations. The decision to merge these schemes underscores a commitment to simplification, consistency, and effectiveness. By consolidating the schemes, the government aims to streamline the process, ensure fair treatment across businesses, and ultimately drive increased investment in innovation. At MPA, we recognize the importance of these changes and stand ready to assist businesses in understanding and leveraging the new opportunities presented.

Contact Us

We specialise in helping businesses fund their innovative ideas and provide tailored modeling to help them navigate changes. Contact us now.

You may be interested in

On The 4th April, 11:00 am – 11:45 am, our expert-led session will demystify the complexities of the merger, highlighting key changes, critical timelines, and what these mean for your R&D claims.

- Tackle common misconceptions head-on

- Gain a broader perspective on how the industry is adapting

- Learn best practices for maintaining quality, compliant claims under the new guidelines

- Learn how to make the process work for you to ensure your R&D claims continue to deliver maximum value

- Have your questions answered

Whether you’re a finance professional, business owner, or just keen to stay informed, this webinar is your stepping stone to making the process work for you despite all the changes in the last 12 months.