Blog: Changes to R&D Tax Credits from August 2023 – Additional Information Form

- R&D Tax Credits

- Innovation

- UK Business

- 9 Min Read

Please be aware that the original date that changes were due to come into effect was the 1st of August 2023. HMRC has delayed the rollout to 8th August 2023. The dates in this article have been updated.

Oh yes, it’s yet another change for the R&D Tax Credit scheme in 2023. Not only will R&D claimants need to be compliant with the changes that came into effect from April 2023, but another amendment to the claim process is due to come into effect from 8th August 2023. Ensure you are prepared for the future of R&D and join our webcast on 25th July at 11am!

From the 8th August 2023, you will need to complete and submit an additional information form to HMRC to support your Research and Development (R&D) Tax Credit claim. Unlike some of the other changes in April 2023, this change will be compulsory for all R&D Tax Credit claims, not just for those who are new to claiming.

So, what do you need to know about the latest change, and what do you need to do to be prepared?

On this page you will learn:

Subscribe to our monthly newsletter, we’ll keep you informed on each of the R&D changes, and provide useful UK business advice and insights into how to fund innovation and business growth.

Subscribe to newsletter

When do you need to submit the additional information form?

The R&D tax credit additional information form must be submitted before you submit your company’s Corporation Tax Return. This will come into effect on 8th August 2023.

If you don’t follow the new process in the order that HMRC requires (before the Corporation Tax Return submission), they will remove your R&D tax relief claim from your company’s Tax Return. This means that your claim may be at risk if you miss this important step.

HMRC have explained that they will confirm in writing if they believe that you have not submitted your additional information form before submitting your Corporation Tax Return.

If you are submitting your R&D Tax Relief claim prior to the 8th of August 2023, you have the option to submit the additional information form prior to the launch date of the 8th of August 2023. Although the changes to the R&D tax credit process do not apply to you this year, you will be required to do so on your subsequent claims.

If you wish to supply the additional information form ahead of the changes to the R&D Tax Credit process in August, there has been no clarity given from HMRC on whether this will benefit your claim in terms of improving the speed and success of your claim, or if it will prevent the likelihood of a compliance check.

Who can submit the R&D Tax Credit additional information form?

There are two options available for how you can provide the additional information in conjunction with your R&D tax relief claim. HMRC states that:

- A representative from the company itself can complete and submit the additional information form.

- The agent, advisor or consultant that is acting on behalf of the company wishing to submit an R&D tax credit claim can complete and submit the additional information.

It is up to you who will fulfil this requirement; however, the information must be accurate and must be submitted before your company’s corporation Return is filed. It is also important if working with an agent to compile your claim that the information on both your additional information form and the R&D claim itself matches.

What information is needed on the form?

- Company Details

You will need to provide your company’s:

-

- Unique Taxpayer Reference (UTR), this must match the one shown in your Company Tax Return

- Employer PAYE reference number

- VAT registration number

- Business type, for example your current SIC (Standard Industrial Classification) code.

- Contact Details

The contact details of:

-

- the main senior internal R&D contact in the company who is responsible for the R&D claim, for example a company director.

- Any agent involved in the R&D claim.

- Accounting period dates

The accounting period start and end date for which you’re claiming the tax relief, this must match the one shown in your Company Tax Return.

- Qualifying Expenditure details

Include details of the qualifying expenditure.

If you meet the conditions, you can claim for either or both:

-

- Tax relief as a small and medium-sized enterprise (SME Scheme)

- Expenditure credit as a large company or SME (RDEC Scheme)

If you’re claiming for SME tax relief, you can claim for:

-

- cloud computing costs, including storage, for accounting periods beginning on or after 1 April 2023

- consumable items, for example materials or utilities

- data licence costs, for accounting periods beginning on or after 1 April 2023

- externally provided workers

- payments to participants of a clinical trial

- software

- staff

- subcontractor costs

If you’re claiming for expenditure credit, you may be able to claim for:

-

- cloud computing costs, including storage, for accounting periods beginning on or after 1 April 2023

- consumable items, for example materials or utilities

- contributions to independent R&D costs

- data licence costs, for accounting periods beginning on or after 1 April 2023

- externally provided workers

- payments to participants of a clinical trial

- software

- staff

- subcontractor costs

- Qualifying indirect activities

On the additional information form, you must include the amount of qualifying expenditure for each project of qualifying indirect activities, that do not directly lead to resolving the uncertainty.

This may include:

-

- creating information services for R&D support such as preparing a report of R&D findings

- direct supporting activities such as maintenance, security, administration and clerical activities and finance and personnel activities, for the share that relates to R&D

- ancillary activities needed to begin R&D, for example taking on and paying staff, leasing laboratories and maintaining R&D equipment, including computers used for R&D purposes

- training required to directly support the R&D project

- research by students and researchers carried out at universities

- research including data collection to make new scientific or technological testing, surveys or sampling methods, where this research is not R&D in its own right

- feasibility studies to inform the strategic direction of a specific R&D activity

This cannot include any costs related to data licensing or cloud computing.

- Project details

The number of all the projects that you’re claiming for in the accounting period and their details.

If you’re claiming:

-

- for 1 to 3 projects, you need to describe all the projects you’re claiming for that cover 100% of the qualifying expenditure

- for 4 to 10 projects, you need to describe those projects that account for at least 50% of the total expenditure, with a minimum of 3 projects described

- for 11 to 100 (or more) projects, you need to describe those projects that account for at least 50% of the total expenditure, with a minimum of 3 projects described — if the qualifying expenditure is split across multiple smaller projects, describe the 10 largest.

How to submit your additional information form?

Once the form has been submitted, you will no longer have access to the information. We advise that you keep a separate copy on record before submitting your additional information form so that you can refer back to this when submitting your R&D Tax Credit claim. The information on the additional information form must match the details in the R&D claim application.

You can submit the form if you’re:

- a representative of the company — you will need the Government Gateway user ID and password you used when you registered for Corporation Tax, if you do not have a user ID, you can create one the first time you sign in

- an agent — you will need the Government Gateway user ID and password you used when you registered for the agent services account, if you do not have a user ID, you can create one the first time you sign in

The additional information form can be submitted here.

You will then get an email to confirm that we’ve received the form, this email will contain a reference number.

Keep a note of this reference number so that:

- you can discuss your additional information form with HMRC

- if HMRC need to, they can check that you’ve submitted your additional information form.

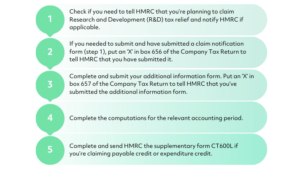

Where does the additional information form fit into the R&D claim process from 8th August 2023?

- Check if you need to tell HMRC that you’re planning to claim Research and Development (R&D) tax relief for accounting periods beginning on or after 1 April 2023. Notify HMRC if applicable. The latest date that you must submit the claim notification form is 6 months after the end of the period of account that the claim relates to.

- If you needed to submit and have submitted a claim notification form (step 1), put an ‘X’ in box 656 of the Company Tax Return to tell HMRC that you have submitted it.

- Complete and submit your additional information form. Put an ‘X’ in box 657 of the Company Tax Return to tell HMRC that you’ve submitted the additional information form.

- Complete the computations for the relevant accounting period.

- Complete and send HMRC the supplementary form CT600L if you’re claiming payable credit or expenditure credit.

Are you ready for the 8th August changes to R&D Tax Credits 2023?

If you need any support in preparing for the changes to the R&D Tax Credit process, we are here to help. As experts in the field for over 16 years, we can offer 1:1 advice on how you can ensure that you have everything ready to comply with the changes.

Sometimes it’s just easier to have a chat. We can help you find the best solution in the quickest possible way. Leave your details below for a callback.

Contact Us